The strong franc is having a dual impact on the Swiss economy: it is holding back inflation and hindering Swiss exports. In such conditions, the SNB might implement currency interventions or cut the interest rate. However, the central bank has not delivered any signals. Let's discuss this topic and make a trading plan for the USDCHF pair.

The article covers the following subjects:

Major Takeaways

- Markets do not expect the SNB to cut rates.

- A strong franc is a problem for exports.

- The Swiss National Bank may surprise the markets.

- Long positions can be opened on the USDCHF pair with a target of 0.805 if the SNB cuts the key rate.

Weekly Fundamental Forecast for Franc

The Swiss National Bank has lulled the currency market into such a state of complacency that the surprise of lowering the key rate below zero at the September 25 meeting will be striking. According to Bloomberg, only two of the 21 experts believe this will happen, which has heightened market volatility.

The SNB, under its new governor, Martin Schlegel, can be described as neither fish nor fowl. While his predecessor, Thomas Jordan, was generous with currency interventions and statements about the franc being overbought, a new broom sweeps clean, but an old broom knows the corners. Despite the Swiss franc's rise to 10-year highs against the euro and the US dollar, the central bank is not concerned about specific levels. What matters to it is pace.

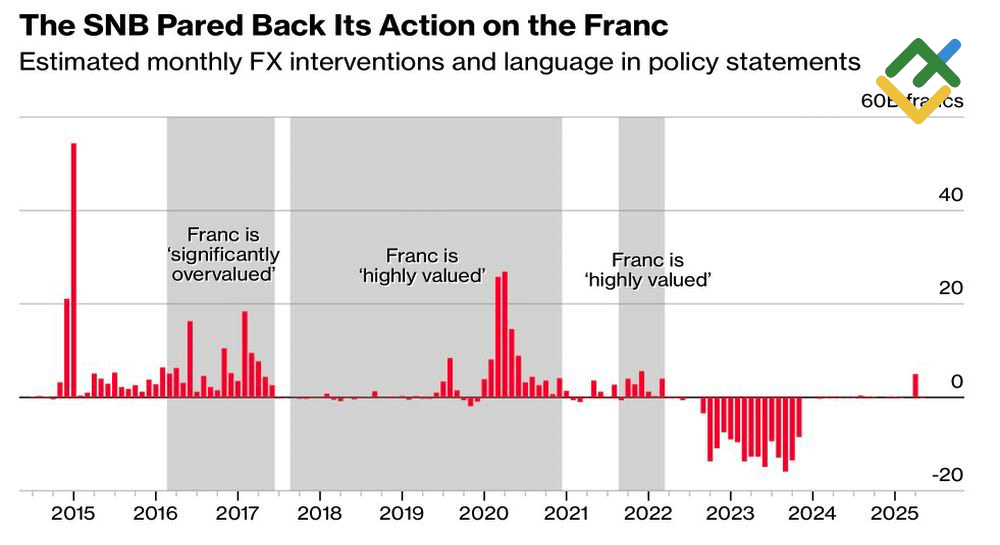

SNB FX Interventions

Source: Bloomberg.

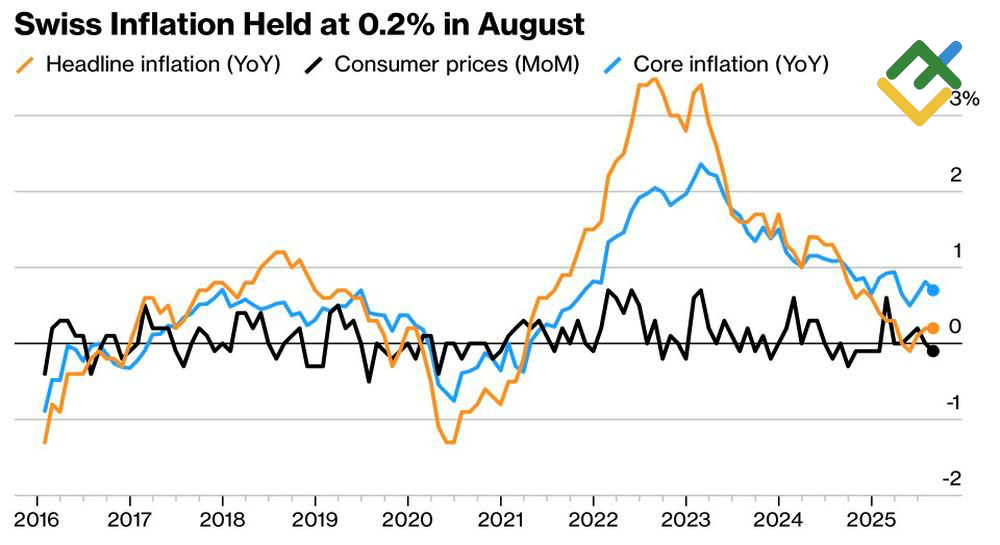

Some say that the Swiss National Bank has run out of options, while others suggest that it hesitates due to the potential repercussions from the US. Thomas Jordan could have lowered the key rate significantly below zero until deflation was under control. Martin Schlegel prefers to discuss the potential negative implications of negative borrowing costs and to provide optimistic price forecasts. Meanwhile, the current CPI is at the lower end of the target range of 0-2%.

Swiss Inflation Change

Source: Bloomberg.

The SNB's shift in perspective is prompting banks and investment firms to reevaluate their forecasts. ING and Nomura believe that the cycle of monetary policy easing in Switzerland has reached its end. Barclays and Capital Economics have adjusted their expectations from September to December. While in August, 7 out of 22 Bloomberg experts anticipated a key rate reduction in September, currently, only 2 out of 21 hold this view.

If the National Bank's objective was to mislead investors into a false sense of security, it has been accomplished. At the same time, the 39% US tariffs could deal a severe blow to Swiss exports. The SNB should provide support by weakening the franc by reducing the key rate.

Morgan Stanley's analysis revealed that, despite meeting less frequently than other regulators, the SNB is the most likely to surprise investors. Furthermore, the Federal Reserve and the Swedish Riksbank's decision to reduce interest rates could provide further support for the easing of monetary policy. Continuing the cycle of monetary expansion will reduce the risks of Switzerland returning to deflation, which the SNB has long fought against in the past.

Weekly USDCHF Trading Plan

As a result, the market anticipates that the key rate will remain at zero in September. However, no decisions have been finalized. A reduction to -0.25% or lower would be a game-changer for the financial markets and would allow the USDCHF pair to soar towards 0.805. On the contrary, the central bank's passivity is a reason to increase previously formed short trades with the targets of 0.776 and 0.75.

This forecast is based on the analysis of fundamental factors, including official statements from financial institutions and regulators, various geopolitical and economic developments, and statistical data. Historical market data are also considered.

Price chart of USDCHF in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.