IEOs and STOs as new forms of initial coin offering. Description of the models, advantages, disadvantages for investors and issuers, prospects

The once-popular option to attract investors, in 2018 ICOs disappointed the issuers. The lack of control led to the emergence of dozens of scam startups, while the collapse of the market caused investors to lose interest in small new projects, thus almost putting an end to ICOs. In order to return investors' interest to the market, in 2019, two new models of initial coin offering were proposed: IEO and STO. IEO is basically ICO, but led by an exchange analyzing the competitiveness of startups. STO is an attempt to turn coint into an asset of the securities market. Read more about these models in the review.

IEO and STO as new ICO forms intended to shake up the market

On the securities market, a joint-stock company that wants to attract investors holds an IPO (Initial Public Offering). IPO has the following stages: full audit of the company, including financial documents and management, marketing campaign and listing with the IPO holder (stock exchange). Listing involves auditors, banks, private brokers, underwriters, lawyers, depositories, etc. Only after jumping through all the hoops will securities get to the stock market to be in free access for outside investors.

There is an analogue of IPO in the cryptocurrency world – ICO (Initial Coin Offering), which includes listing a startup coin with a cryptocurrency exchange to attract investors. However, after the purchase of coins, investors do not get ownership of the startup and there aren't so many participants involved in it. In 2018-2019, new cryptocurrency offering options appeared to protect the interests of investors – IEO and STO.

In this review you will learn:

- What IEO is and it differs from ICO.

- How ICO and IEO are held. What the advantages and disadvantages of IEO for investors are.

- What STO is and what its prospects are.

IEO – investor protection or a new scam?

A cryptocurrency startup wishing to attract investors' money has two options: ICO and attracting funds by themselves. In order to save money (as they need to pay for listing, auditing, etc.), some developers resorted to the second option. Social networks, specialized forums, word of mouth – they used all the marketing ways to attract potential investors to the platform website, where they found a wallet waiting for them with detailed instructions on how to download it, install it, and buy the coins (presale or crowdsale).

- Pre-sale, as deduced from the name, is the preliminary sale of coins. Crowdsale is the main sale of coins through the platform's website. This core stage is often called ICO. But such offerings are difficult to account in statistics, and it is impossible to determine the real price of the coin. In addition, they are often simply a pyramid. As a confirmation of the reliability of the startup, its coins are listed on the exchange. But in order to be listed, a startup needs to meet a number of conditions. In this review, ICO is defined as the placement of coins on the exchange.

The model of selling coins via the website, which can be described as a sort of crowdfunding, was efficient in 2017 when the market was growing at an amazing pace. After the emergence of a series of pyramids and dummy startups, investors became more prudent and the ICO era began. According to ICORating, in 2017, 6.1 billion US dollars were raised via ICOs, while only in the first quarter of 2018, the figure was about 6.9-7 billion US dollars.

Marketers quickly dubbed ICO «new IPO», though forgetting to clarify a number of details. For example:

- During an IPO, the company must obtain a regulator's approval (in particular, in the United States). No regulators are involved in ICOs.

- In an IPO, the exchange risks its reputation, being under the control of the regulator. There are no regulators in the cryptocurrency world, and exchanges go bankrupt every day, unlike the stock market.

- During an IPO, the company fully discloses information about its operations. This definitely cannot be said about cryptocurrency platforms. We saw many instances when there were photos of strangers in the section “About the team” on the startup's website.

The idea worked. Investors believed that ICO is a much more reliable investment option. Indeed, in theory, ICO means additional costs for developers. If developers have money, there is hope that the startup is not a scam. The ICO model itself seemed convincing too.

Interesting fact: there are dozens of articles online with instructions on “How to hold an ICO”, but you will not find any such articles on IPOs. This makes sense. To hold an IPO, you need to use resources that are not comparable with the resources required for ICO. This is why the developers jumped at yet another idea of luring gullible investors: only about 30-50% of the money was spent on developing platforms, the rest went to pay for listing and aggressive marketing. Trusting investors, in turn, supported developers without going into the essence of ICO.

Poor consequences of ICOs for investors

In 2018, Statis Group consulting firm held a study that assessed the life cycle of startups launched in 2017 using ICO. Projects were analyzed from the first presale on the project’s website until the coins appeared on cryptocurrency exchanges. These are the results of the study:

- 81% of startups showed all the signs of a scam. These are not only the pyramids but also startups that are unlikely to become real companies.

- About 70% of the startups that emerged were funded by investors despite the signs of a scam.

The figures, although approximate (you can find many similar studies), allow you to imagine the scale of the disaster.

In 2018, the situation was even worse:

- In November and December, ICO startups managed to attract about $65 and $55 million, respectively. For comparison: in January and February, the figures were $2.4 and $2.6 billion, followed by a downtrend. In the next 3 months, they managed to attract an average of $2 billion, from July to August – $1 billion each month. Although there is an opinion that the reason is a decrease in capitalization, it is rather simple: investors were disappointed in the ICOs and preferred coins from the TOP list that had existed for more than a year.

- According to EY, 86% of the most notable coins that had ICOs in late 2017 – early 2018 were worth less than at the time of offering.

- According to Cointelegraph, by the end of the year, 19% of the projects that had ICOs already deleted their websites.

In total, they managed to attract 12.2 billion US dollars in 2018, of which 1.7 billion were for Telegram and 4.2 billion – for EOS. According to analysts, 46.6% of the startups that held ICOs did not have a starting product (i.e., the startup only had a website and a development plan). 26.2% had a viable product, 15.5% of the developers only offered the alpha version, 11.2% – the beta version. 0.5% had ICOs with only source code.

According to TokenData, in the first quarter of 2019, ICO projects attracted only 118 million US dollars.

The developers would create a shell startup, enter the market, raise money, and then see how it goes. Is it a scam? Probably not. At least in comparison with 2017, the number of pyramids decreased in 2018, which explains the increased initial interest of investors in ICOs. But after most platforms remained shells, investors grew more rational.

IEO as an ICO replacement

After the ICO model stopped attracting investors, the developers decided to offer a different model for bringing startups to the market – IEO (Initial Exchange Offering). In theory, the task of this model is to filter new startups and its main difference from ICO is the bigger role of the exchange in this process.

IEO is the initial offering of coins on the exchange. In this case, the role of the organizer goes from the developer to the exchange. Differences from ICO:

- With ICO, the developer does all the marketing. They use paid advertising, forums, social media. With IEO, the exchange assumes this role.

- With ICO, the exchange only provides a platform and includes the coin in the list on a paid basis. This means , a stock exchange is only an intermediary not accountable to investors for potential scam. With IEO, the exchange assesses the project, attracts investors and manages the offering of coins.

Coin issuers (developers) pay a listing fee to the exchange along with the percentage of coins sold during the offering. Investors do not send money through a smart contract (as in ICO), but rather create an account with the exchange and deposit money to exchange wallets. In other words, with IEO, all transactions go through the exchange that verifies both issuers and investors.

An investor enters into a sort of contract with the exchange, the terms of which may differ. For example, it may contain restrictions on the number of coins bought per person. This eliminates the centralization problem and the possibility of a 51% attack. The exchange does a full audit and assessment of issuers, thereby carrying reputational risks.

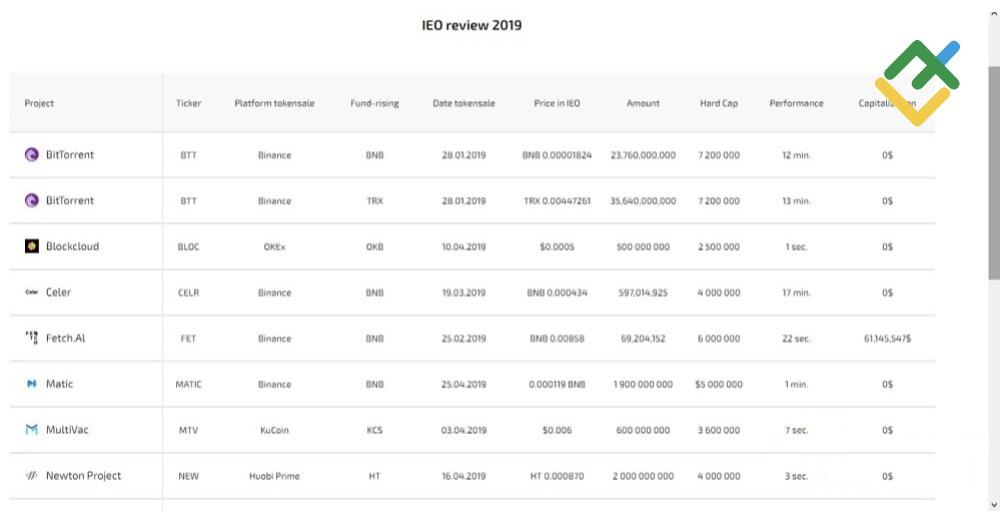

Example. In April 2019, Huobi added a condition for investors: only those who had at least 500 TH on their accounts for the past 30 days could take part in the IEO (Huobi Token are internal exchange tokens used to buy issuer tokens). Thus, the exchange tried to limit the number of users who bought out the entire issues of tokens in several minutes in previous token sales.

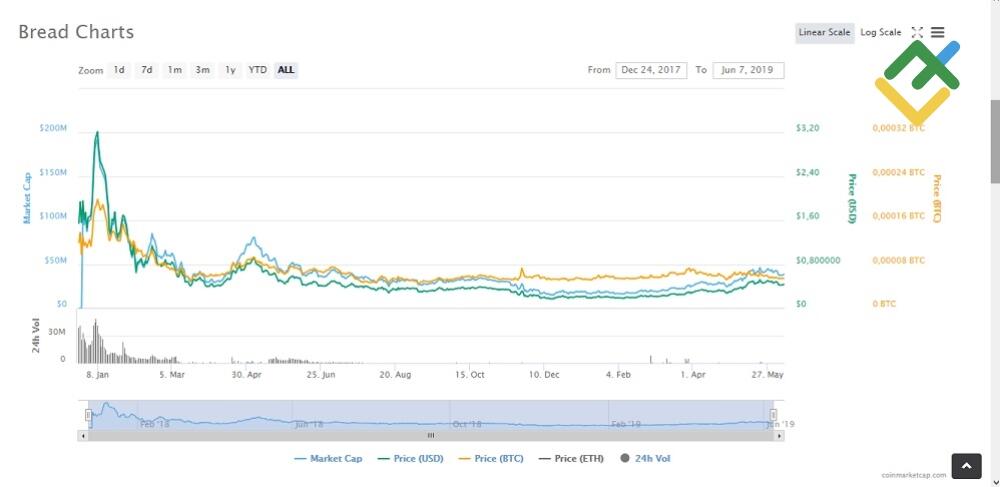

The IEO model was first tested by the Binance exchange at the end of 2017, which launched its own platform called the Binance Launchpad using this model. The first startups were GIFTO and BREAD. In February 2019, the exchange held the offering of TRON’s BitTorrent tokens. All three projects collected more than 15 million dollars in the first few minutes. Seeing the success of Binance, other exchanges, including Huobi (Huobi Prime and Huobi Prime Lite platforms) and OKEx (OK Jumpstart platform), reported on launching their own platforms for IEO.

In March and April, the first IEOs also took place at other exchanges. For the first quarter of 2019, according to various estimates, the capitalization of startups on these platforms amounted to 0.8-1.0 billion dollars, but the number of token sales remains a little over than two dozen. Binance promises to hold at least one IEO per month, the plans of other exchanges are unknown. It is also worth noting that new startups are not doing so great.

In theory, IEO has one significant advantage – unviable startups with unfinished code will not get listed on the stock exchange and rating resources. Such startups can still sell their tokens through their own website, but it is unlikely to be of interest to investors.

IEO benefits:

- Concentration of strong promising startups on major exchanges. Coin offering is costly, and developers prefer to work with major exchanges with a reputation and a permanent user base. Small exchanges that aim to make money without providing guarantees do not usually hold IEOs.

- Investors save time. With ICO, an investor had to search for interesting startups across the Internet, while with the IEO model they just go to the exchange website and see the calendar of future offerings. I can draw an analogy with buying a car: ICO is like searching the entire market with the risk of buying a defective car. IEO is like going to the car dealer, where the supply is smaller than on the car market, but you can be confident that the car is brand new.

- Developers (issuers) also save time. IEO is also associated with saving money, but this is a mistake: the marketing budget simply goes to the stock exchange.

In theory, the IEO model looks convincing to investors: TOP exchanges filter bad startups.

The first quarter of 2019 showed that investors welcomed the new investment model, and issuers resumed the development of startups. But this model is still not perfect.

IEO disadvantages:

- For the issuer, it means additional costs. In addition to marketing costs and listing, the issuer will pay for the assessment and in some cases a percentage of the amount raised.

- For the investor, it means the requirement to pass verification. The exchange have had the verification procedure before, but it is expected to become more strict.

- Legal uncertainty remains in the procedure for attracting investor funds. So far, each exchange has its own IEO terms for both parties, and there are no uniform principles for resolving disputes and conflicts. ICOs had the same problem, and the exchange doesn't really protect the interests of investors.

Despite the initial success of the model, the forecast for its prospects is rather pessimistic for several reasons:

- Difference between scams and dummies. Even if we assume that the stock exchange actually assesses startups in good faith, it can only filter out evident scams. Almost all startups holding IEOs are in their seed stage and raise money to continue development. In practice, nothing prevents them from freezing the project after collecting money, after which the price of the token will go down. A similar situation was observed in the ICO model.

- The myth about the reputational liability of the exchange for scams. The cryptocurrency community saw hundreds of scams, hacks, and scandals involving exchanges. Did it affect their reputation? Not really. Sometimes there were local outflows of investor capital, but in general, the situation has not changed. Therefore, it is unlikely that exchanges will evaluate startups scrupulously, which means that investors should again prepare to see a lot of dummies.

- Biased exchanges. There are no strict criteria for evaluating startups. The exchanges can screen out really interesting projects only because they could not provide an attractive commercial offer and give priority to those that will be beneficial to them contrary to the interests of issuers and investors.

- Technical implementation of the idea. The first try was not that successful. When Fetch.AI startup was offering tokens with Binance, only 2,700 users out of 20,000 who participated in the IEO were able to buy the token. The situation repeated with the Celer token, where only 3,100 out of 39,000 people became investors. Huobi has a similar problem. Even without launching the Huobi Prime platform, the exchange announced the launch of Huobi Prime Lite with an accelerated listing process and a flexible asset allocation process.

Despite the fact that by June 2019 only about 15-20 IEOs were held, it couldn't go without a scandal. 15 minutes before its first IEO of the RAID startup in March 2019, Bittrex canceled the offering. The reason was the suspicion of fraud, but the situation turned out to be more complicated.

How to invest in IEO

In comparison with the procedure, the issuer has to go through to get to the exchange to, becoming an investor is quite easy:

- Go to the exchange website and find its supporting platform for IEOs.

- Browse the calendar of offerings, register, pass verification in accordance with the requirements of the exchange.

- Deposit, invest.

If you didn’t find an interesting startup or have no desire to pass verification, there is always the opportunity to invest in startups using the ICO model. But the risks, then, will lie entirely with the investor.

There is an opinion that IEO is the beginning of reformatting of the cryptocurrency market. People argue that the number of new startups will now decrease, but they will be more reliable, while the dummies disappear. I'm not so sure. Nor am I sure that IEOs will be able to change the situation drastically.

Not IPO, but not ICO either. Will STO be a compromise for the cryptocurrency community and regulators?

The STO model also appeared recently as an alternative to ICO. It is a serious step to make coins a real financial instrument instead of just something ethereal (as viewed by many people). In this model, the problem of legislative compliance of cryptocurrency with the requirements of the stock market has been partially solved, which means that cryptocurrencies may soon be on par with the assets of the commodity, stock and currency markets.

The model is as follows. ICO provides for the production of coins, let's call them "classic tokens". The SEC (USA) and FINMA (Switzerland) regulators proposed a slightly different classification of emitted tokens:

- Payment Tokens – tokens for the payment for platform services, this is internal currency of a startup that allows you to get a product offered by developers.

- Utility Tokens – tokens used for additional platform options, auxiliary tokens.

- Security Tokens or tokenized securities.

The first two types of tokens do not fall under regulation, but the third type (STO) does.

Security Tokens are digital assets subject to federal securities laws, a cross between classic tokens and financial products. They certify ownership and give the owner the right to the result of investment goals: a per cent of profits or dividends. Rights are recorded in smart contracts, and the tokens can be traded on exchanges.

The STO model solves several structural issues:

- Eliminates the problem of guaranteeing compensation in case of fraud by the issuer (developer).

- Provides an opportunity to hedge risks: accredited investors can buy tokens after the project is launched on the basis of a previously concluded Simple Agreement for Future Token (SAFT).

- Partially solve the problem of integrating cryptocurrencies into the natural financial environment and the problem of legislative regulation.

- Banks and similar intermediary companies are excluded from the chain of counterparties. This reduces transaction costs and increases market liquidity.

Investment tokens must be registered same as traditional securities. In this case, the issuer undertakes the obligation to comply with the securities legislation, including possible legal proceedings.

However, in this advantage lies the first problem of the STO model. In order to comply with the requirements of the legislation, the issuer must invest time and money (this is a sort of IPO). And while the volume of stock market turnover allows outweighing these costs, the cryptocurrency turnover in the conditions of investor scepticism is not so big yet. If ICO can be carried out with insignificant costs, STO threatens to catch up with IPO in terms of costs, which levels the advantage of blockchain.

The second problem is that anonymity will be a thing of the past. Even if a startup holds private offering without registering the issue, in the eyes of the regulator the issue will not be anonymous. I see this as a positive aspect, but supporters of anonymity of transactions (investors with unrecorded capital) may not love this idea.

And finally, the third problem is the limited access of investors to the offering. Since STO must meet the requirements of the SEC, only accredited investors can become participants, i.e.investors with an annual income of 200,000 dollars for individuals, and with assets over 1 million dollars ex real estate for legal entities.

In 2018, only about 4-5% of developers took the risk to issue coins using this model. A few examples of such startups are Angenium (app created on the basis of Ethereum) and Blockestates (Polymath platform). There aren't many exchanges working with this kind of asset. Binance and NASDAQ announced their desire to adopt the system in 2019, in January, the tZero platform (a subsidiary of the global online retailer Overstock.com) was launched with KODAKCoin as the first token.

Conclusion.

IEO is a new version of coin offering under the strict control of the exchange, a replacement for the ICO model that failed in 2019. This model is designed to protect the market from scam startups and, in theory, it should be more attractive to investors than ICO. But:

- The number of startups entering the market using the IEO model is still very small. There are practically none to choose from and only 10-15% of IEO participants manage to buy the desired tokens. Perhaps in the future, the number of IEOs will increase. But given the need to verify startups, growth is unlikely to be substantial.

- The exchange assessing the startup does not guarantee its existence in the future. The risks of an investor with IEO remain almost the same as with ICO: developers may stop supporting the project; the price of the token may fall below the purchase price due to the total market capitalization decline.

- There are requirements for investors: minimum account balance during a fixed period, more stringent verification.

So far, the IEO model is not working out great and it seems that this is a new ICO model created in order to return investors' confidence and interest in minor and young startups.

The STO digital asset model seems more promising due to several factors:

- Reliability. Tokens are subject to financial laws.

- It solves regulatory issues and protects the interests of investors.

Despite the fact that there are not many tokens released using this model, it seems to be viable and might potentially make a profit in the long run.

I would recommend investors to be cautious, monitor new projects and new trends on the market, but give preference to the classic coins from the TOP 20. If you have experience investing in new projects or would like to express your opinion about ICOs, IEOs and STOs, I invite you to join the discussion in the comments!

P.S. Did you like my article? Share it in social networks: it will be the best "thank you" :)

Useful links:

- I recommend trying to trade with a reliable broker here. The system allows you to trade by yourself or copy successful traders from all across the globe.

- Use my promo code BLOG to get a 50% deposit bonus on the LiteFinance platform. Simply enter this code in the appropriate field when funding your trading account.

- Telegram chat for traders: https://t.me/litefinancebrokerchat. We are sharing the signals and trading experience.

- Telegram channel with high-quality analytics, Forex reviews, training articles, and other useful things for traders https://t.me/litefinance

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.