Why banks attract deposits: the role of banks in economic system, whether the high interest rates are real. What negative interest rate is and why it appears.

A common answer that comes up first is that banks attract deposits, give loans and earn money from it. It is partially so, but then, why do banks offer different interest rates, which are radically different in different countries? Since recently, there has been a common practice when a depositor pays a fee to a bank for a keeping deposit, and the borrower receives compensation from the bank, rather than repays an interest on the debt. How could it be? You will learn from the article about the role of banks and bank deposits in the whole macroeconomic system, why banks need money in general and what the negative interest rate is.

Bank deposits: purpose, value for banks and macroeconomics

The answer seems obvious: banks attract deposits, make loans and gain money from the difference between loan rates and deposit rates. Usual funds distribution in the economic environment. However, everything is not that simple. For example, have you noticed that in some countries deposit rates are higher than loan rates?

Yes, it is about deposits for individuals and targeted loans for legal entities. But still a fact takes place. And in some countries the situation is even more interesting, deposit interest rates are negative! That is, those who invest money in deposits now also have to pay for keeping them in the bank. But the borrowers are satisfied.

For example, in Denmark, banks also pay a premium to mortgage borrowers (the interest for the use of the loan is not charged). It seems incredible, doesn’t it? In fact, everything is quite reasonable.

In this review, I’ll try to answer the following questions:

- Why do banks need deposits and what functions do the banks perform in general in the money turnover?

- Why do banks offer different interest rates on deposits and should you trust high deposit rates?

- Where did the concept of negative interest rates come from, and why don’t some banks need our money?

And, of course, if you still have questions or want to study how the banking system works, I’m looking forward to your comments!

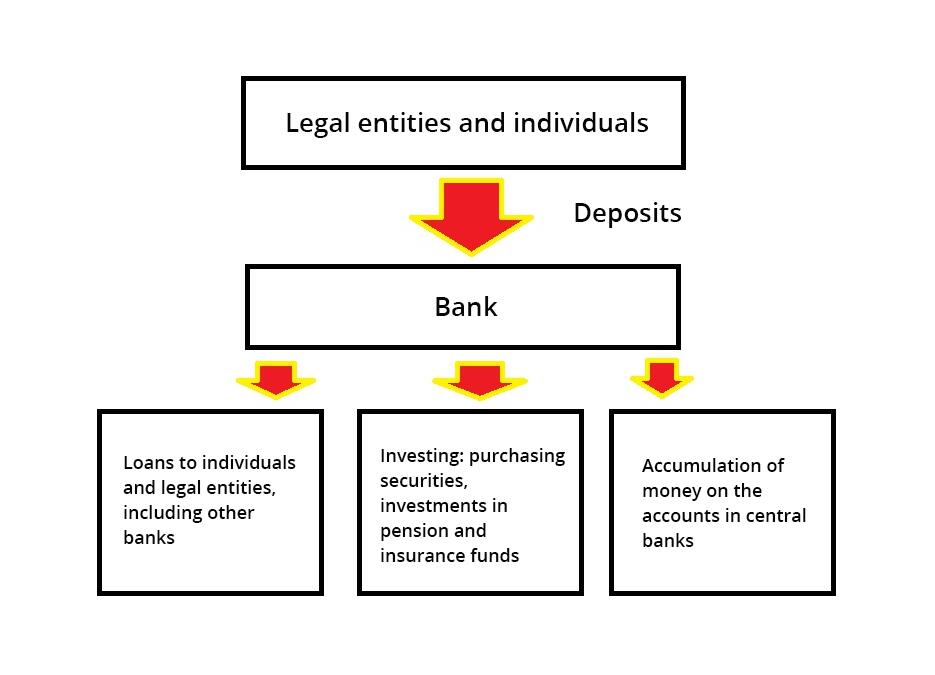

Banks and people: circulation of money

Banks play the part of an intermediary in the financial services market. Simply put, they accumulate money from some sources and redistribute it to other sources.

Sources of money for the bank are deposits of legal entities and individuals, income from cash and settlement operations (transaction services), from investments in various types of assets, including securities, income from lending to individuals and legal entities, and other banks. Banks can redistribute the money in loans, investments (purchase of securities, derivatives), deposits in other banks, including central banks, etc.

1. Intermediary in the money cycle

Everything is simple here: the bank attracts the money of those who have spare funds, paying them premium in the form of interest, and distributes it to those areas that generate it profit, covering the costs of deposit servicing. One could say that banks thereby stimulate the development of the national economy, supporting loans and investment companies. But everything serves to a single purpose – make profits.

Deposit interest rate depends in a way on how much a banks wants to get the depositor’s money. And the key factor is its strategy. For example, as experience proves, the loan interest rates are higher for retail short-term collateral-free loans (this is because of their higher risk level). Accordingly, a bank aimed at retail lending will offer higher deposit rates. If the bank has an appropriate risk management system, then the probability of losing the deposit will be insignificant.

Why does the bank needs the depositor's money? To make loans. But there can be a different situation: to cover the holes in the balance sheet. I’ll give an example from real life. In one country, there was a mortgage boom at some point. It was more profitable to take real estate loans in foreign currency due to lower interest rates in the equivalent, and the loans, of course, were long-term. Therefore, those who took loans in foreign currency were completely surprised when their loans increased by three times after the local currency’s value was set free.

There started mass payment failures and challenging credit contracts. Banks had to cover the foreign exchange difference from their own income reserves. Attempts to sell the mortgaged property, estimated at the previous exchange rate, did not solve the problem. As a last resort, banks raised deposit interest rates, hoping to solve the liquidity problem at the expense of investors. However, the investors themselves subject to panic quickly withdrew their deposits. The outcome was logical: about 1/3 of the banks that could not close the balance gap were closed.

Something like this was in the USA in 2008. At that time the bank needed the money of depositors and investors to fund new mortgage loans. They issued mortgage-backed securities (a type of security), which were said to be funded by the loans, and sold them to investors. Conclusion: high interest rates on deposits may suggest potential problems of the bank.

There is another remarkable moment. If a bank offers a high deposit interest rate it doesn’t always mean that the bank needs your money. It may need exactly you. Attracting clients, the bank also tries to impose on them other types of services: loans and credit cards, payroll projects, underwriter services, issuing guarantees, selling precious metals, brokerage services, value storage services, etc.

2. Support of their own liquidity

Bank assets are grouped according to the terms. Simply put, the bank needs to maintain instant overdrafts, short-term consumer loans, issue long-term loans, have sufficient cash reserves, etc. Therefore, the bank’s liabilities have a structural division into the time range. In order to maintain short, middle and long-term liquidity, the bank may change deposit interest rates. For example, to provide higher interest rates on short-term deposits or, on the contrary, to attract long-term deposits without the right of early withdrawal for long-term loans.

It also should be added that the bank may that the bank may need money to provide the liquidity coverage ratio and capital adequacy, demanded by the central banks. Sometimes, there may be minor cash gaps, that is, a shortage of money in the short term. They can borrow money on the interbank market or conduct repo transactions. Or they can raise deposit interest rates.

3. Participation in monetary system

One of the central bank’s functions is to provide the appropriate money supply. Simply put, if at a certain level of production in the country there is a lot of local currency, prices will be higher, if there is little of it, prices will go down. Too much money – high inflation, too little money - overheating of the economy. Both states set back the economic development of the country. Therefore, advanced economies set the target inflation rate. For example, the target inflation of 2% annually is in the USA and Japan.

One of the monetary policy tools is affecting the interest rates on deposits and loans by changing the discount rate:

- If the central bank wants to strengthen the national currency, it increases the interest rate. First, the currency becomes more appealing for foreign investors. Second, the interest rate on deposits and loans automatically increase. That is because when the central bank and commercial banks need your money, they raise the interest rates. People prefer deposits to consumption, and so, the money supply is reduced in the money turnover, curbing the inflation rate.

- If a country lacks money supply (insufficient liquidity) the central bank, on the contrary, pumps the country with currency through commercial banks. Banks cut deposit interest rates (why do they need individuals’ deposits if its cheaper to take a loan form the central bank?), and so, the credit interest rates also go down, which increases the money supply in the country's turnover.

A short summary. Banks need our money:

- To earn money on making loans and other financial operations

- To attract clients for cash and settlement services, where deposits are only a part of integrated package of services;

- To fill the economy with liquidity in order to develop production and services industry

It seems to be clear why banks need clients’ money. But there some exceptions when the situation is a little different.

The rich also suffer

While in emerging markets, banks make every effort to attract depositors, in the advanced economies, the situation is opposite. What do the banks in developed countries need our money for? Nothing! They would be eager to abandon deposits, but people themselves are willing to deposit their money, setting their country’s economy back.

In the 2000s, such countries as Great Britain, Japan, the EU countries and and these in the Scandinavian Peninsula faced an interesting phenomenon:

- Frightened by a series of bankruptcies and defaults, commercial banks stopped issuing loans, preferring a money-saving policy. It was especially prominent after 2008. Even the term “liquidity trap” was introduced, meaning that banks, attracting deposits, did not distribute them to lending, preferring to keep them on the accounts in the central bank. Accordingly, the interest rates on deposits went down.

- The population, whose mentality is aimed at money safekeeping money, continued to deposit money in banks. The idea of capital accumulation is very close to thrifty Germans, Swedes, and Danes. But money must work, otherwise the economy will not develop.

As it has been written above, roughly outlined, people deposit their money in banks, banks make loans for development, production, updating and improvement of technologies and equipment. If people keep their money in the bank, the consumer demand declines (it is logical since people already have everything they need. Why should they buy one more car if they can keep their money in the bank? Enterprises that do not receive loans reduce production. Insufficient development and upgrading of technologies eventually leads to structural economic problems.

There is another factor. A strong national currency is unprofitable for exporters, because their revenue is in a foreign currency, but they buy raw materials and labor for the money of their country. The leading central banks of advanced economies faced both of these problems.

In 2009, the Swiss National Bank for the first time introduces negative interest rates on its sight deposit account balances, thus forcing commercial banks to pay for deposits. “A fee for keeping money” - the same way went commercial banks in relation to individuals. The goal of the central bank was to make money work by means of the monetary policy tool; it should run in the economy, bringing added value, rather than lay on bank accounts.

In the 2011-2012, Swiss example was followed by other advanced economies (Denmark, Sweden, Bulgaria, Japan, Hungary). The result was unexpected:

- In Denmark and Sweden, they managed to weaken the national currency, thereby supporting exporters. In Denmark, there was even a situation when banks paid to their borrowers on condition of mortgage lending (the interest rate for the loan was not charged).

- German banks faced an outflow of funds from deposits of individuals, but the demand for safes increased. So, they could hardly make the residents invest their money in stocks, for example, or investment funds.

- In Japan, negative interest rates didn’t do at all. Investors see the yen as a safe heaven to invest in during the turmoil in financial markets. The inflation target was not reached and the yen remained strong.

An alternative to negative interest rates (which didn’t make the impact expected everywhere) became an idea of “helicopter money”. The term was coined by a Nobel Prize Winner Milton Friedman in 1969. The basic principle is that if a central bank wants to raise inflation and output in an economy that is running substantially below potential, one of the most effective tools would be simply to give everyone direct money transfers, excluding banks from the chain of quantitative easing. In 2016, in Switzerland, where negative rates did not make expected effect, this idea was discussed at a referendum. This is an amazing fact for developing countries: 77% of people refused to get for free an average of 2,300 euros per adult and 570 euros per child.

There are opponents of the negative interest rate policy. They argue that negative interest rates will on the contrary encourage people to save up money as a spare safety funds. Much depends on whether the pension funds are state or private. The monetary structure is also important. In Sweden, where about 2% of cash is left in the financial system (that is, everything goes through the banks), the idea of negative rates is working. In Switzerland, where this share is more than 10%, it turned out to be more profitable to keep cash at home than in banks.

Another concern is that the attempts to abandon public money and expand lending may lead to more unreliable borrowers. However, each country has its own monetary system. And as you can see from the examples above, some banks need money, and some do not. It all depends on many particular factors. Economists themselves sometimes do not know what will be the result of a particular experiment.

Conclusion.

Deposits are not just a tool of banks to gain money on the subsequent making loans. Deposits and loans are only a part of the country’s monetary system that provides fair distribution of resources among all its participants by different means, including the central bank’s guidance. The central bank mostly determines what interest rates on deposits are offered by banks.

How common depositors can use it:

- Do not hurry to make a deposit at too attractive interest rates. It may be a last resort of a bank before bankruptcy.

- Do not deceive yourself, thinking that when you deposit your money in a bank you, even if indirectly, take part in the country’s economic development. Just because your money isn’t kept under your pillow but works to the benefit of the country. If the interest rate of course higher than zero.

- Look for alternative sources of income.

The latter advice amidst negative interest rates or rates not covering inflation in emerging markets seems to be the most reasonable. You can store you money in a safe just as well, but it is better to increase your capital by other means. In the recent times, banks are rather for quick transactions and brokerage (managing) services, as well as for regulating the money supply in the country. That is why, it is more yielding to make money in stock markets, commodity markets or on currency exchange rates. The stock market or over-the-counter-market will suit best here. However, for those who are willing to freeze their money for a long time with a potential yield of up to 100% of annual return, I suggest the article about investments of the future.

What about you? Are you for bank deposits or against? Please, do write your comments under the article!

P.S. Did you like my article? Share it in social networks: it will be the best "thank you" :)

Useful links:

- I recommend trying to trade with a reliable broker here. The system allows you to trade by yourself or copy successful traders from all across the globe.

- Use my promo code BLOG to get a 50% deposit bonus on the LiteFinance platform. Simply enter this code in the appropriate field when funding your trading account.

- Telegram chat for traders: https://t.me/litefinancebrokerchat. We are sharing the signals and trading experience.

- Telegram channel with high-quality analytics, Forex reviews, training articles, and other useful things for traders https://t.me/litefinance

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.