Gold has not yet returned to its pre-war levels, unlike stock indices and major global currencies. It continues to factor in the risks of accelerating global inflation and slowing economic growth. Let's discuss this topic and make a trading plan for XAU/USD.

The article covers the following subjects:

Major Takeaways

- The rally in the S&P 500 is supporting gold.

- The precious metal is no longer concerned about rising interest rates.

- Central banks are unlikely to sell their gold reserves.

- A rebound from 4,730 and 4,690 is a buying opportunity for XAU/USD.

Weekly Fundamental Forecast for Gold

Throughout history, investors have allocated capital across various assets, but they have always come back to gold. After using the precious metal as a source of liquidity to meet margin requirements in stocks in March, investors resumed buying XAU/USD in April amid the S&P 500's sharp rally. This factor, combined with easing concerns about further monetary tightening by major central banks, is driving gold higher.

The conflict in the Middle East created an unfavorable backdrop for gold. Rising oil prices were expected to fuel inflation and push central banks to raise interest rates. Before the bombing of Iran, futures markets were pricing in two rounds of monetary easing from the Fed and the Bank of England, while expecting the ECB to keep borrowing costs unchanged through the end of 2026. The war shifted investor expectations. The Fed's inaction, two rate hikes from the Bank of England, and three from the ECB laid the groundwork for XAU/USD selling in March.

In April, the situation reversed completely. According to Andrew Bailey, the Bank of England is in no rush to raise the repo rate. The ECB is also taking a cautious approach, according to Bloomberg sources. New York Fed President John Williams believes the current Fed stance is well-balanced to address risks related to both inflation and unemployment. As a result, gold is no longer concerned about aggressive monetary tightening and has moved higher.

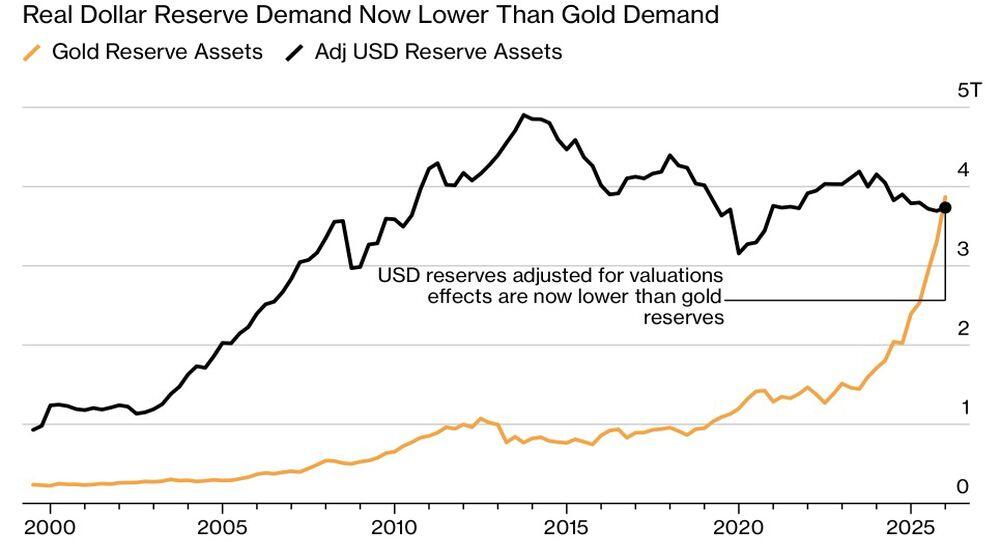

Dynamics of Gold and US Dollar Shares in Central Bank Reserves

Source: Bloomberg.

Despite global monetary tightening in 2022–2023, gold continued to rise due to ongoing de-dollarization and reserve diversification by central banks. As a result, gold's share in global reserves surpassed that of US dollar assets for the first time since records began in 1990.

There were concerns that the Middle East conflict could reverse this trend. Some countries were expected to start selling gold reserves to support weakening economies and currencies. Fortunately, the ceasefire between the US and Iran has restored confidence in a lasting peace, putting those fears to rest.

At this stage, gold appears to be one of the most logical choices for investors. If equity and currency markets have already priced in the end of the war and returned to the levels seen before the bombing of Iran, or even exceeded them, XAU/USD is still trading about 9% below its pre-bombing levels. The precious metal still factors in stagflation risks that other assets have chosen to ignore. At the same time, accelerating inflation amid a cautious Fed is likely to work in gold's favor. In such conditions, real Treasury yields are expected to decline. Combined with a weaker US dollar, this creates an ideal environment for gold.

Weekly Trading Plan for XAU/USD

Under these conditions, XAU/USD's rebound from the 4,730 and 4,690 support levels, or a move back above 4,840, can be used to open long positions. The main risk to this outlook is a renewed escalation of the conflict in the Middle East.

This forecast is based on the analysis of fundamental factors, including official statements from financial institutions and regulators, various geopolitical and economic developments, and statistical data. Historical market data are also considered.

Price chart of XAUUSD in real time mode

The content of this article reflects the author’s opinion and does not necessarily reflect the official position of LiteFinance broker. The material published on this page is provided for informational purposes only and should not be considered as the provision of investment advice for the purposes of Directive 2014/65/EU.

According to copyright law, this article is considered intellectual property, which includes a prohibition on copying and distributing it without consent.